迴歸診斷¶

此範例檔案展示如何在實際情境中使用幾個 statsmodels 迴歸診斷檢定。您可以在迴歸診斷頁面上了解更多關於檢定的資訊。

請注意,這裡描述的大多數檢定只會回傳一個數字的元組,而沒有任何註解。輸出的完整描述始終包含在 docstring 和線上 statsmodels 文件中。為了呈現的目的,我們使用 zip(name,test) 結構在下面的範例中漂亮地印出簡短的描述。

估計迴歸模型¶

[1]:

%matplotlib inline

[2]:

from statsmodels.compat import lzip

import numpy as np

import pandas as pd

import statsmodels.formula.api as smf

import statsmodels.stats.api as sms

import matplotlib.pyplot as plt

# Load data

url = "https://raw.githubusercontent.com/vincentarelbundock/Rdatasets/master/csv/HistData/Guerry.csv"

dat = pd.read_csv(url)

# Fit regression model (using the natural log of one of the regressors)

results = smf.ols("Lottery ~ Literacy + np.log(Pop1831)", data=dat).fit()

# Inspect the results

print(results.summary())

OLS Regression Results

==============================================================================

Dep. Variable: Lottery R-squared: 0.348

Model: OLS Adj. R-squared: 0.333

Method: Least Squares F-statistic: 22.20

Date: Thu, 03 Oct 2024 Prob (F-statistic): 1.90e-08

Time: 16:05:44 Log-Likelihood: -379.82

No. Observations: 86 AIC: 765.6

Df Residuals: 83 BIC: 773.0

Df Model: 2

Covariance Type: nonrobust

===================================================================================

coef std err t P>|t| [0.025 0.975]

-----------------------------------------------------------------------------------

Intercept 246.4341 35.233 6.995 0.000 176.358 316.510

Literacy -0.4889 0.128 -3.832 0.000 -0.743 -0.235

np.log(Pop1831) -31.3114 5.977 -5.239 0.000 -43.199 -19.424

==============================================================================

Omnibus: 3.713 Durbin-Watson: 2.019

Prob(Omnibus): 0.156 Jarque-Bera (JB): 3.394

Skew: -0.487 Prob(JB): 0.183

Kurtosis: 3.003 Cond. No. 702.

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

殘差的常態性¶

Jarque-Bera 檢定

[3]:

name = ["Jarque-Bera", "Chi^2 two-tail prob.", "Skew", "Kurtosis"]

test = sms.jarque_bera(results.resid)

lzip(name, test)

[3]:

[('Jarque-Bera', np.float64(3.39360802484318)),

('Chi^2 two-tail prob.', np.float64(0.18326831231663254)),

('Skew', np.float64(-0.4865803431122347)),

('Kurtosis', np.float64(3.003417757881634))]

Omni 檢定

[4]:

name = ["Chi^2", "Two-tail probability"]

test = sms.omni_normtest(results.resid)

lzip(name, test)

[4]:

[('Chi^2', np.float64(3.7134378115971933)),

('Two-tail probability', np.float64(0.15618424580304735))]

影響力檢定¶

一旦創建完成,類別為 OLSInfluence 的物件會持有屬性和方法,讓使用者評估每個觀察值的影響力。例如,我們可以透過以下方式計算並提取 DFbetas 的前幾列

[5]:

from statsmodels.stats.outliers_influence import OLSInfluence

test_class = OLSInfluence(results)

test_class.dfbetas[:5, :]

[5]:

array([[-0.00301154, 0.00290872, 0.00118179],

[-0.06425662, 0.04043093, 0.06281609],

[ 0.01554894, -0.03556038, -0.00905336],

[ 0.17899858, 0.04098207, -0.18062352],

[ 0.29679073, 0.21249207, -0.3213655 ]])

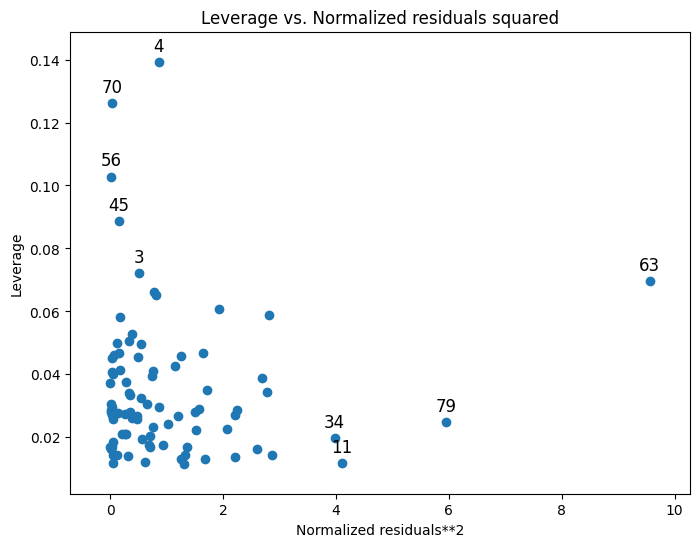

輸入 dir(influence_test) 來探索其他選項

關於槓桿作用的有用資訊也可以繪製出來

[6]:

from statsmodels.graphics.regressionplots import plot_leverage_resid2

fig, ax = plt.subplots(figsize=(8, 6))

fig = plot_leverage_resid2(results, ax=ax)

其他繪圖選項可以在繪圖頁面上找到。

多重共線性¶

條件數

[7]:

np.linalg.cond(results.model.exog)

[7]:

np.float64(702.1792145490066)

異質變異數檢定¶

Breush-Pagan 檢定

[8]:

name = ["Lagrange multiplier statistic", "p-value", "f-value", "f p-value"]

test = sms.het_breuschpagan(results.resid, results.model.exog)

lzip(name, test)

[8]:

[('Lagrange multiplier statistic', np.float64(4.893213374094005)),

('p-value', np.float64(0.08658690502352002)),

('f-value', np.float64(2.5037159462564618)),

('f p-value', np.float64(0.08794028782672814))]

Goldfeld-Quandt 檢定

[9]:

name = ["F statistic", "p-value"]

test = sms.het_goldfeldquandt(results.resid, results.model.exog)

lzip(name, test)

[9]:

[('F statistic', np.float64(1.1002422436378143)),

('p-value', np.float64(0.38202950686925324))]

線性¶

Harvey-Collier 乘數檢定,用於檢定線性規格是否正確的虛無假設

[10]:

name = ["t value", "p value"]

test = sms.linear_harvey_collier(results)

lzip(name, test)

[10]:

[('t value', np.float64(-1.0796490077759802)),

('p value', np.float64(0.2834639247569222))]

上次更新:2024 年 10 月 03 日