在狀態空間模型中估計或指定參數¶

在本筆記本中,我們展示如何在估計其他參數的同時,固定 statsmodels 狀態空間模型中某些參數的特定值。

一般而言,狀態空間模型允許使用者

透過最大似然估計所有參數

固定某些參數並估計其餘參數

固定所有參數(使不估計任何參數)

[1]:

%matplotlib inline

from importlib import reload

import numpy as np

import pandas as pd

import statsmodels.api as sm

import matplotlib.pyplot as plt

from pandas_datareader.data import DataReader

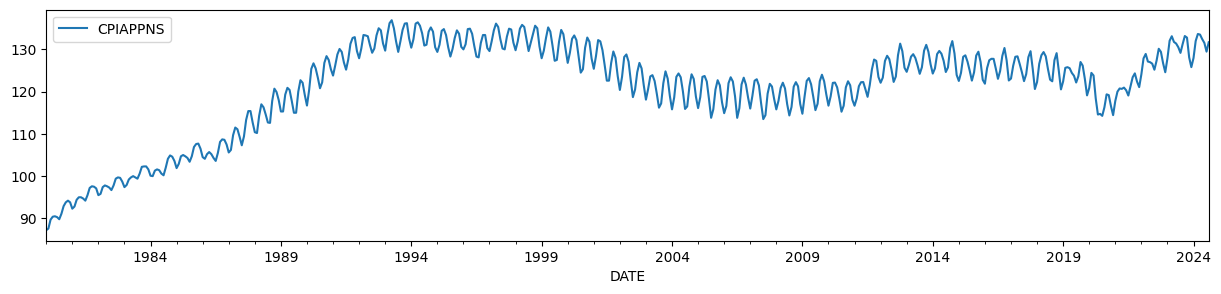

為了說明,我們將使用服裝的消費者物價指數,該指數具有隨時間變化的水平和強烈的季節性成分。

[2]:

endog = DataReader('CPIAPPNS', 'fred', start='1980').asfreq('MS')

endog.plot(figsize=(15, 3));

眾所周知(例如,Harvey 和 Jaeger [1993]),HP 濾波器的輸出可以由未觀察到的成分模型產生,只要對參數施加某些限制。

未觀察到的成分模型為

為了使趨勢與 HP 濾波器的輸出相匹配,必須按如下方式設定參數

其中 \(\lambda\) 是關聯的 HP 濾波器的參數。對於我們在此使用的每月數據,通常建議使用 \(\lambda = 129600\)。

[3]:

# Run the HP filter with lambda = 129600

hp_cycle, hp_trend = sm.tsa.filters.hpfilter(endog, lamb=129600)

# The unobserved components model above is the local linear trend, or "lltrend", specification

mod = sm.tsa.UnobservedComponents(endog, 'lltrend')

print(mod.param_names)

['sigma2.irregular', 'sigma2.level', 'sigma2.trend']

未觀察到的成分模型 (UCM) 的參數寫為

\(\sigma_\varepsilon^2 = \text{sigma2.irregular}\)

\(\sigma_\eta^2 = \text{sigma2.level}\)

\(\sigma_\zeta^2 = \text{sigma2.trend}\)

為了滿足上述限制,我們將設定 \((\sigma_\varepsilon^2, \sigma_\eta^2, \sigma_\zeta^2) = (1, 0, 1 / 129600)\)。

由於我們在此固定所有參數,因此完全不需要使用 fit 方法,因為該方法用於執行最大似然估計。相反,我們可以透過使用 smooth 方法,直接在我們選擇的參數下執行 Kalman 濾波器和平滑器。

[4]:

res = mod.smooth([1., 0, 1. / 129600])

print(res.summary())

Unobserved Components Results

==============================================================================

Dep. Variable: CPIAPPNS No. Observations: 536

Model: local linear trend Log Likelihood -2997.309

Date: Thu, 03 Oct 2024 AIC 6000.619

Time: 15:45:23 BIC 6013.460

Sample: 01-01-1980 HQIC 6005.643

- 08-01-2024

Covariance Type: opg

====================================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------------

sigma2.irregular 1.0000 0.009 115.621 0.000 0.983 1.017

sigma2.level 0 0.000 0 1.000 -0.000 0.000

sigma2.trend 7.716e-06 1.98e-07 38.962 0.000 7.33e-06 8.1e-06

===================================================================================

Ljung-Box (L1) (Q): 254.28 Jarque-Bera (JB): 1.58

Prob(Q): 0.00 Prob(JB): 0.45

Heteroskedasticity (H): 2.21 Skew: 0.04

Prob(H) (two-sided): 0.00 Kurtosis: 2.75

===================================================================================

Warnings:

[1] Covariance matrix calculated using the outer product of gradients (complex-step).

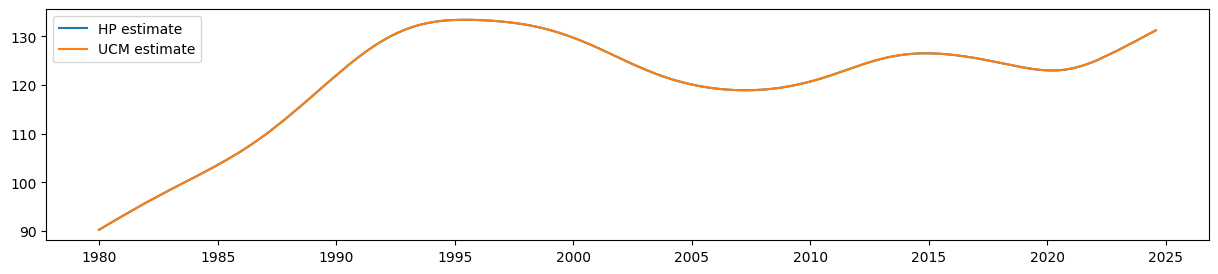

與 HP 濾波器趨勢估計值相對應的估計值,由 level 的平滑估計值給出(在上面的符號中,即為 \(\mu_t\))

[5]:

ucm_trend = pd.Series(res.level.smoothed, index=endog.index)

很容易看出,來自 UCM 的平滑水平估計值等於 HP 濾波器的輸出

[6]:

fig, ax = plt.subplots(figsize=(15, 3))

ax.plot(hp_trend, label='HP estimate')

ax.plot(ucm_trend, label='UCM estimate')

ax.legend();

加入季節性成分¶

然而,未觀察到的成分模型比 HP 濾波器更具彈性。例如,上面顯示的數據明顯具有季節性,但季節性影響隨時間變化(開始時的季節性比結束時弱得多)。未觀察到的成分架構的好處之一是,我們可以加入隨機季節性成分。在這種情況下,我們將透過最大似然估計季節性成分的變異數,同時仍包含上述參數上的限制,以便趨勢與 HP 濾波器的概念相對應。

加入隨機季節性成分會加入一個新參數 sigma2.seasonal。

[7]:

# Construct a local linear trend model with a stochastic seasonal component of period 1 year

mod = sm.tsa.UnobservedComponents(endog, 'lltrend', seasonal=12, stochastic_seasonal=True)

print(mod.param_names)

['sigma2.irregular', 'sigma2.level', 'sigma2.trend', 'sigma2.seasonal']

在這種情況下,我們將繼續如上所述限制前三個參數,但我們希望透過最大似然估計 sigma2.seasonal 的值。因此,我們將使用 fit 方法以及 fix_params 環境管理器。

fix_params 方法會接收參數名稱和關聯值的字典。在產生的環境中,這些參數將在所有情況下使用。在 fit 方法的情況下,只會估計未固定的參數。

[8]:

# Here we restrict the first three parameters to specific values

with mod.fix_params({'sigma2.irregular': 1, 'sigma2.level': 0, 'sigma2.trend': 1. / 129600}):

# Now we fit any remaining parameters, which in this case

# is just `sigma2.seasonal`

res_restricted = mod.fit()

RUNNING THE L-BFGS-B CODE

* * *

Machine precision = 2.220D-16

N = 1 M = 10

At X0 0 variables are exactly at the bounds

At iterate 0 f= 3.87642D+00 |proj g|= 2.27476D-01

At iterate 5 f= 3.25868D+00 |proj g|= 2.20983D-06

* * *

Tit = total number of iterations

Tnf = total number of function evaluations

Tnint = total number of segments explored during Cauchy searches

Skip = number of BFGS updates skipped

Nact = number of active bounds at final generalized Cauchy point

Projg = norm of the final projected gradient

F = final function value

* * *

N Tit Tnf Tnint Skip Nact Projg F

1 5 12 1 0 0 2.210D-06 3.259D+00

F = 3.2586810226319427

CONVERGENCE: NORM_OF_PROJECTED_GRADIENT_<=_PGTOL

This problem is unconstrained.

或者,我們也可以直接使用 fit_constrained 方法,該方法也接收約束字典

[9]:

res_restricted = mod.fit_constrained({'sigma2.irregular': 1, 'sigma2.level': 0, 'sigma2.trend': 1. / 129600})

RUNNING THE L-BFGS-B CODE

* * *

Machine precision = 2.220D-16

N = 1 M = 10

At X0 0 variables are exactly at the bounds

At iterate 0 f= 3.87642D+00 |proj g|= 2.27476D-01

At iterate 5 f= 3.25868D+00 |proj g|= 2.20983D-06

* * *

Tit = total number of iterations

Tnf = total number of function evaluations

Tnint = total number of segments explored during Cauchy searches

Skip = number of BFGS updates skipped

Nact = number of active bounds at final generalized Cauchy point

Projg = norm of the final projected gradient

F = final function value

* * *

N Tit Tnf Tnint Skip Nact Projg F

1 5 12 1 0 0 2.210D-06 3.259D+00

F = 3.2586810226319427

CONVERGENCE: NORM_OF_PROJECTED_GRADIENT_<=_PGTOL

This problem is unconstrained.

摘要輸出包含所有參數,但指出前三個參數已固定(因此未進行估計)。

[10]:

print(res_restricted.summary())

Unobserved Components Results

=====================================================================================

Dep. Variable: CPIAPPNS No. Observations: 536

Model: local linear trend Log Likelihood -1746.653

+ stochastic seasonal(12) AIC 3495.306

Date: Thu, 03 Oct 2024 BIC 3499.566

Time: 15:45:24 HQIC 3496.974

Sample: 01-01-1980

- 08-01-2024

Covariance Type: opg

============================================================================================

coef std err z P>|z| [0.025 0.975]

--------------------------------------------------------------------------------------------

sigma2.irregular (fixed) 1.0000 nan nan nan nan nan

sigma2.level (fixed) 0 nan nan nan nan nan

sigma2.trend (fixed) 7.716e-06 nan nan nan nan nan

sigma2.seasonal 0.0924 0.007 12.672 0.000 0.078 0.107

===================================================================================

Ljung-Box (L1) (Q): 459.85 Jarque-Bera (JB): 38.49

Prob(Q): 0.00 Prob(JB): 0.00

Heteroskedasticity (H): 2.44 Skew: 0.30

Prob(H) (two-sided): 0.00 Kurtosis: 4.19

===================================================================================

Warnings:

[1] Covariance matrix calculated using the outer product of gradients (complex-step).

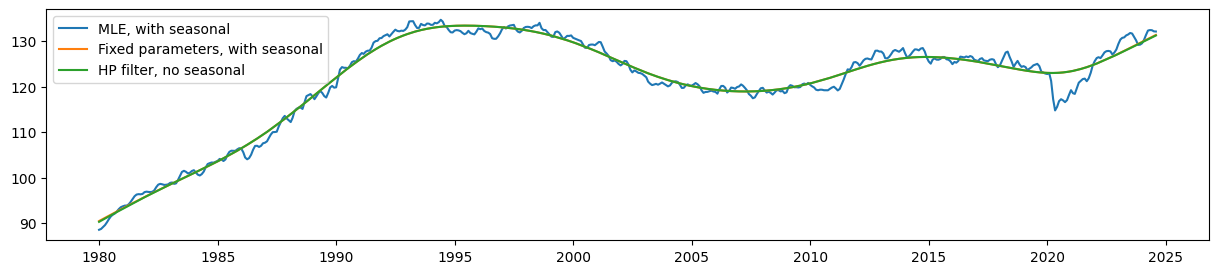

為了進行比較,我們建構了不受限制的最大似然估計 (MLE)。在這種情況下,水平的估計值將不再對應於 HP 濾波器的概念。

[11]:

res_unrestricted = mod.fit()

RUNNING THE L-BFGS-B CODE

* * *

Machine precision = 2.220D-16

N = 4 M = 10

At X0 0 variables are exactly at the bounds

At iterate 0 f= 3.63596D+00 |proj g|= 1.07339D-01

This problem is unconstrained.

At iterate 5 f= 2.03169D+00 |proj g|= 4.05225D-01

ys=-5.696E-01 -gs= 2.818E-01 BFGS update SKIPPED

At iterate 10 f= 1.59907D+00 |proj g|= 7.62230D-01

At iterate 15 f= 1.44540D+00 |proj g|= 2.77893D-01

At iterate 20 f= 1.39111D+00 |proj g|= 1.56723D-01

At iterate 25 f= 1.38688D+00 |proj g|= 1.41002D-03

* * *

Tit = total number of iterations

Tnf = total number of function evaluations

Tnint = total number of segments explored during Cauchy searches

Skip = number of BFGS updates skipped

Nact = number of active bounds at final generalized Cauchy point

Projg = norm of the final projected gradient

F = final function value

* * *

N Tit Tnf Tnint Skip Nact Projg F

4 28 58 1 1 0 2.548D-06 1.387D+00

F = 1.3868826049230436

CONVERGENCE: NORM_OF_PROJECTED_GRADIENT_<=_PGTOL

最後,我們可以擷取趨勢和季節性成分的平滑估計值。

[12]:

# Construct the smoothed level estimates

unrestricted_trend = pd.Series(res_unrestricted.level.smoothed, index=endog.index)

restricted_trend = pd.Series(res_restricted.level.smoothed, index=endog.index)

# Construct the smoothed estimates of the seasonal pattern

unrestricted_seasonal = pd.Series(res_unrestricted.seasonal.smoothed, index=endog.index)

restricted_seasonal = pd.Series(res_restricted.seasonal.smoothed, index=endog.index)

比較估計的水平,很明顯,具有固定參數的季節性 UCM 仍然會產生一個非常接近(雖然不再完全)HP 濾波器輸出的趨勢。

同時,來自沒有參數限制模型(MLE 模型)的估計水平比這些平滑得多。

[13]:

fig, ax = plt.subplots(figsize=(15, 3))

ax.plot(unrestricted_trend, label='MLE, with seasonal')

ax.plot(restricted_trend, label='Fixed parameters, with seasonal')

ax.plot(hp_trend, label='HP filter, no seasonal')

ax.legend();

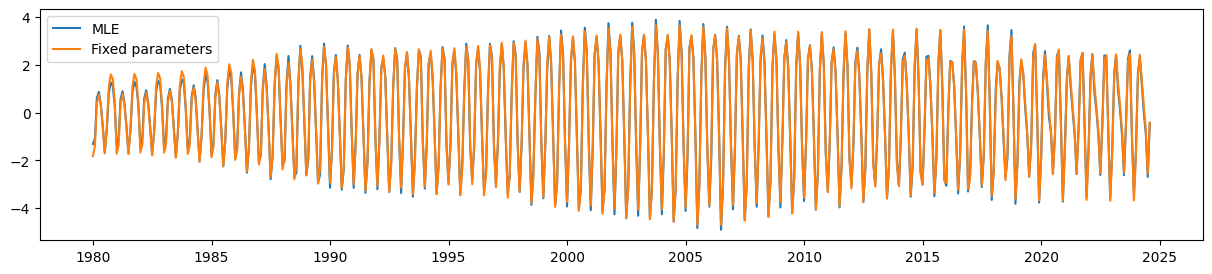

最後,具有參數限制的 UCM 仍然能夠很好地拾取隨時間變化的季節性成分。

[14]:

fig, ax = plt.subplots(figsize=(15, 3))

ax.plot(unrestricted_seasonal, label='MLE')

ax.plot(restricted_seasonal, label='Fixed parameters')

ax.legend();